The article discusses the growth and challenges of the steel industry in India. It highlights India’s position as the second-largest steel producer globally and the need to increase per capita steel consumption. The article also delves into the various challenges faced by the steel sector and outlines mitigation plans to address them.

Since steel was first made in the 17th century, it has been the most consumed alloy in the world. Known for its lightweight and high tensile strength, steel finds application in a wide range of industries – construction, railways, automobiles, capital goods, consumer durables and a wide range of intermediary products.

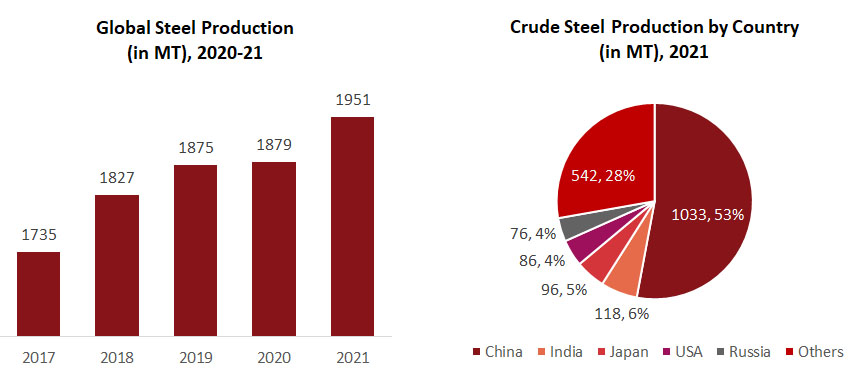

Global steel production has been on a steady growth path – production rose to 1,951 MT in 2021 (3.8% over 2020).

Source: World Steel Association, World Bank

India is the 2nd largest producer of steel in the world behind China, with a total production of 118 MT in 2021. China alone contributes to more than 50% of the world’s total steel production.

India’s growth story in the steel sector has been in line with the global trajectory. Over the past 5 years, the public sector contributed to about 20% of India’s total production, led by Steel Authority of India Limited (SAIL). Private sector production has been led by Tata Steel. However, despite the historic growth in production, per capita consumption of steel in India remains quite low compared to the global average. India’s per capita steel consumption has risen to 77 kg (50% increase in the last 8 years), while the global average stands at 233 kg. China, which has been known for intense infrastructure spending in the past couple of decades, has a per capita consumption of more than 600 kg. Given the pace of infrastructure development in India and the rise of steel-consuming industries like automobiles and capital goods, there is tremendous space for the growth of steel consumption in India.

Source: World Steel Association, World Bank

The National Steel Policy (NSP), introduced by the government in 2017, aims to achieve steel production of 255 MT by 2030, translating to a per capita steel consumption of 160 kg. The industry needs to grow by a CAGR of 9% from 2021 to 2030.

Although there are differences in the efficiency levels of public and private sector across different areas, both sectors need to work together to achieve this target.

Recently in 2021, the government launched Production Linked Incentive (PLI) schemes to incentivise production of speciality steels. Perhaps one of the most important steps undertaken by the government was placing an Anti-Dumping Duty (ADD) on Chinese steel products, which has provided some boost to domestic players that otherwise could not have competed in price with Chinese steel.

While one might assume India has all the right resources including availability of iron ore, skilled workers and most importantly government support, there are challenges the industry faces.

Challenges faced by the Indian steel industry:

- Relatively high cost of financing. Compared other major nations, the cost of financing in India is very high and this continues to be a disadvantage for Indian steel manufacturers. A greenfield project to produce 1 tonne of steel requires an investment of INR 7,000 crore. The high upfront capital cost means almost all projects are financed. India’s current REPO rate is 6.5% compared to China’s rate which ranges between 2-2.5%. According to an assessment report by Niti Ayog, this is leading to a disadvantage of $30-35 dollar per tonne of steel produced.

- Poor logistics and infrastructure: Both raw material and finished goods are heavy bulk materials requiring transportation. To produce 1 tonne of steel, 3-3.5 tonnes of raw material is required. According to a report released by Ministry of Railways in 2021, India has one of the highest freight costs in the world. Indian Iron Ore freight rates are 500% higher compared to Australia, which translates to higher costs for steel producers. Further, India’s plants are mostly situated inland, increasing dependence on road and rail transportation networks which are not adequate or well-equipped enough to promptly dispatch finished products to consumption centers. It is due to this reason that plants closer to the coast prefer buying raw materials from overseas. According to a statement by a Federation of Indian Chambers of Commerce & Industry (FICCI) official, customers bear an additional last mile delivery cost of INR 8,000/tonne, which translates to approximately 28% of factory cost.

- High taxes, duties and cesses increase the cost of doing business. Royalty on Iron Ore in India is one of the highest in the world (15% compared to the global average of 3%-7%). Clean Energy Cess and Customs Duty on raw materials such as coking coal are few examples of additional costs Indian steel manufacturers bear.

- Limited domestic availability of coking coal. Currently, about 68% of Indian steel plants use blast furnace technology, which requires coking coal to produce steel. Based on a report by Ministry of Coal, 90% of the 60 million tons of coking coal required by the steel industry is met through imports. There is potential to decrease this by 25-35% via blending domestically available coking coal. However, the challenge remains in designing complex coal washing infrastructure to clean coal that can be utilized by steel makers.

- High energy consumption: Energy consumption by the industry is second only to the chemical industry. In general, Indian steel manufacturers have higher specific energy consumption, 6-6.5 GCal/tcs, compared to world average of 4.5-5.0GCal/tcs.

Source: Ministry of Steel

| Cost Disadvantage of Indian Steel Industry (USD/ton) | |

| Logistics & Infrastructure | 25 to 30 |

| Power | 8 to 12 |

| Import Duty on Coal | 5 to 7 |

| Clean Energy Cess | 2 to 4 |

| Taxes & Duties on Iron Ore | 8 to 12 |

| Finance | 30 to 35 |

| Total Cost disadvantage | 80 to 100 |

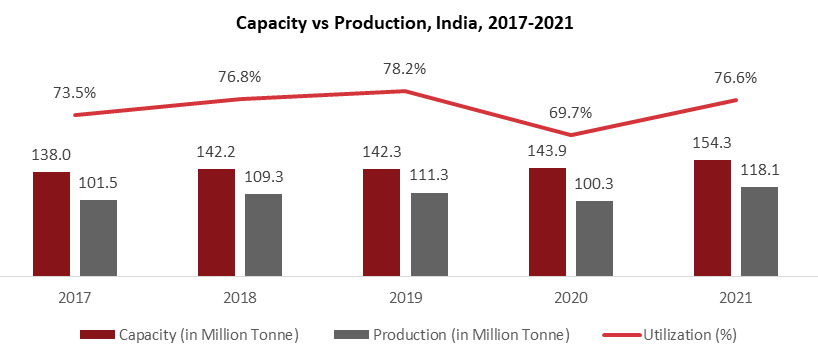

It must be noted that even with these challenges, the Indian steel industry had an utilization of 77% in 2021, which is set to be improved to 85% as per NSP in 2030. The above challenges are cumulatively leading to Indian producers facing a cost disadvantage estimated to be between USD 80-100/tonne compared to global competitors. Financing and “logistics and infrastructure challenges account for USD 55-65/tonne of this disadvantage.

It is important for the industry (public & private) and government to work together to reduce these costs in an aim to compete with China and become competitive in the international market.

Bibhu Prasad Nayak

Bibhu Prasad is a management consultant with specific interest in manufacturing. He has worked with clients on performance improvement, cost optimization, new market entry strategy projects. Other than consulting, Bibhu has worked with companies in the mining, banking, and logistics sectors.

Monojit Roy

Monojit Roy has worked with clients across various industries on projects that include commercial due diligence, customer experience improvement, market, and operational feasibility study. Prior to joining management consulting, he gained experience in engineering consulting and the heavy manufacturing industry, specifically within the nuclear energy and oil & gas sectors.